Forms You May Be Asked to Sign That Have Nothing to Do With Your Offer

Let’s face it, there can be both excitement and anxiety when you’re making an offer on a new house. With all of that emotion, it’s so important to understand what you’re being asked to sign and how it affects the offer you're making to the seller.

Very similar to when you’re signing the paperwork to buy a new car, there may be several documents that your real estate broker/agent presents to you offering a list of additional settlement services that they’d like to sell you. These services have nothing to do with the offer that you’re making to the seller to buy their house, so don’t feel pressured to sign anything. Once the seller has actually agreed to sell you their house you can make a final decision as to who you’d like to hire to provide these services.

Specifically, we’re referring to two disclosures that are sometimes incorporated into one document. Whether they're separate documents or combined, we suggest that you not sign either of them, not yet anyway. By signing them at this time you could be waiving your right to shop around for these services and that move could cost you up to $1,000 or more in unnecessary fees.

- Conveyancing/Broker’s Services Addendum asking you to pay an administration fee for providing a specific list of settlement services.

- Affiliated Business Disclosure is legal notice of a profit sharing agreement with third party real estate service providers. If your real estate broker, agent or lender participates in these types of arrangements, they are required by federal law to disclose it to you.

If your lender or real estate agent suggests that you use the in-house service providers, ask them to provide written quotes for the services but let them know you'll be comparing multiple quotes before making a final decision.

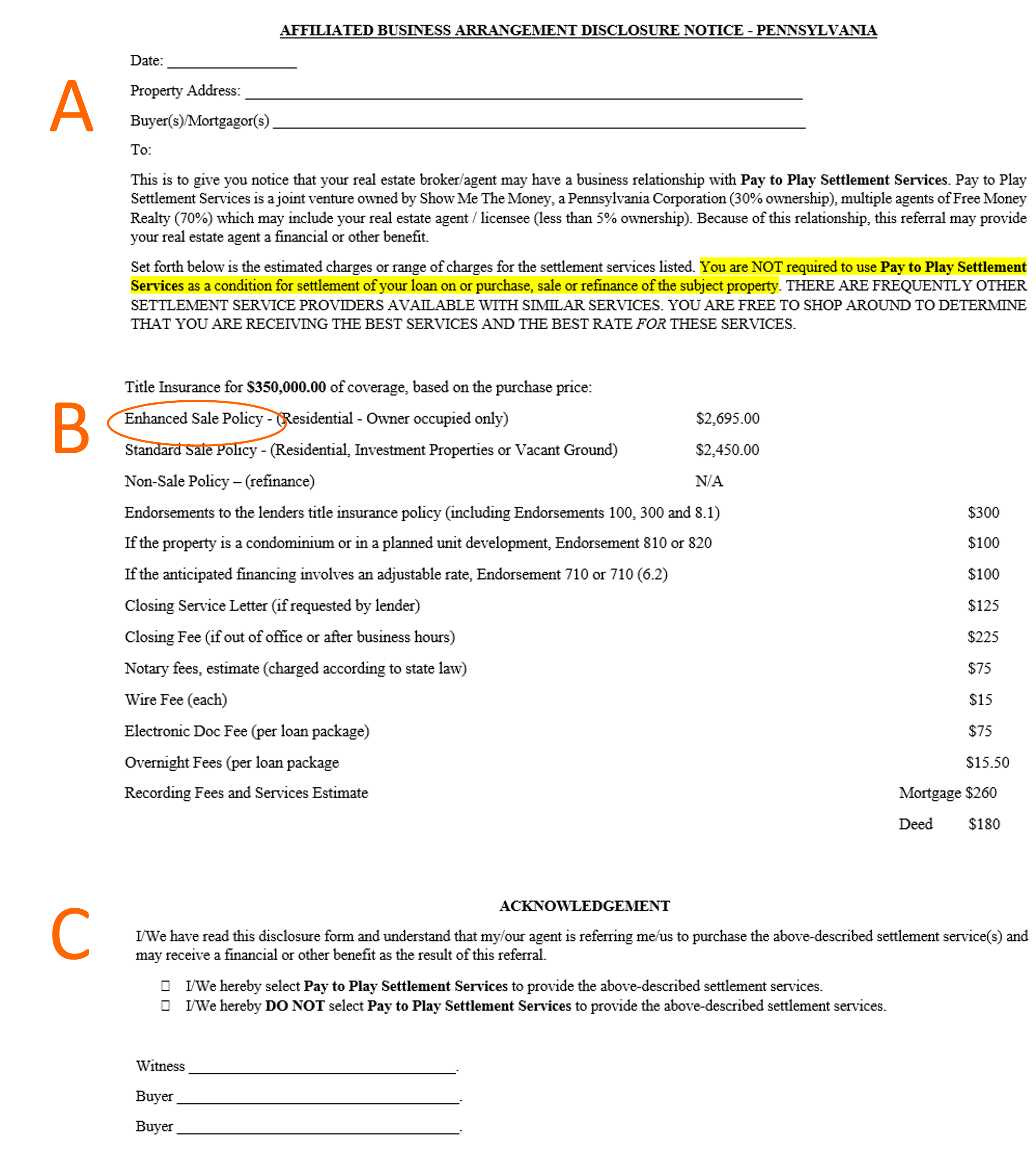

Here's a closer look at a typical Affiliated Business Disclosure that you may be asked to sign.

See the sample Affiliated Business Disclosure below pertaining to Title Insurance and Settlement Services.

Section A reveals who they are affiliated with and what their ownership interest is.

Section B refers to the cost of the title insurance policy and related services.

Section C could be more than just your acknowledgement that you received the disclosure. By checking the wrong box, you may be locking yourself in to using your agent's in-house title company and/or other service providers. If you plan on shopping around before committing to anything, don't sign this form. Once again, it has nothing to do with your offer.

Do I need the Enhanced Title Insurance Policy?

It's also worth noting, in section B, that this particular real estate brokerage quotes the Enhanced Home Owner's Title Insurance Policy by default. While the enhanced coverage might make sense for a small subset of buyers, based on the characteristics of their individual property, the enhanced coverage may not be worth the additional expense for the average buyer.

Tip: When trying to determine if the enhanced policy coverage is right for you, here are a few things to keep in mind:

- The enhanced policy costs 10% more than the standard policy

- An enhanced policy is subject to limitations and deductibles

- Your mortgage lenders only requires standard coverage

- Approximately 85% of the cost differential goes to the person or agency selling you the policy.

We explain standard vs enhanced title policies coverage further on our blog. If after considering both options you feel that the enhanced policy isn’t necessary for your situation, don’t buy it.