THE ALT TITLE HOME BUYER'S GUIDE TO SAVINGS

5 Strategies for minimizing out-of-pocket closing costs and maximizing allowable credits to save thousands more.

ALT works with local lenders and real estate professionals to turn home buyers into homeowners. We set out on a mission to make buying a home more affordable and what we started 20 years ago is quickly becoming the industry standard. Buying a home doesn't have to deplete your savings account. We're going to share with you the same common sense tips we give our customers, friends and family.

It's the right way - the smart way - to buy a house.

1. Ask your lender for a Closing Cost Credit.

With a lender credit towards closing costs, you could possibly offset thousands of dollars in fees.

Lender credits towards allowable closing costs are common and can significantly reduce the amount of cash you’ll need for settlement.

A lender credit sometimes, but not always, comes with a slightly higher mortgage interest rate. However, if preserving the amount of cash you’ll still have in the bank after you buy the house is important to you, the trade-off might be worth it.

Tip: We suggest interviewing with several local lenders or mortgage brokers to compare rates, fees and service. An experienced loan officer or broker will take a look at your income, expenses, and savings and determine what type of loan program best suits your goals. Once that’s been determined, they’ll work with you and your real estate professional to structure your offer once you’ve found the perfect house.

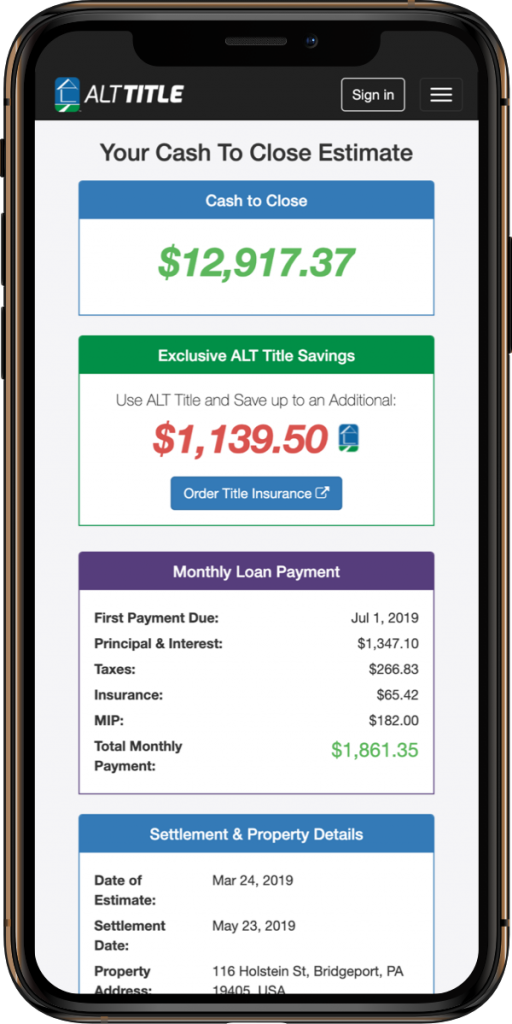

The Ultimate DIY Closing Cost Calculator

2. Choose your own Title Insurance/Settlement Company.

By shopping around for title insurance and settlement services, you can save up to $1,000 or more by eliminating unnecessary settlement related fees.

The old way… real estate brokers, agents and mortgage lenders enter into profit sharing arrangements with title insurance companies where they receive 35%-50% of the title insurance premium as compensation, while their customers are stuck paying inflated and unnecessary fees for settlement services.

Real estate done right… local real estate brokers, agents, mortgage lenders and independent title insurance companies work together to promote home ownership by eliminating confusing business relationships and kickbacks that increase the cost of buying a home. By collaborating with service providers who are committed to putting the customer's financial interests first, more transactions make it to settlement, benefiting everyone.

“It’s just not possible to offer the customer the best deal on real estate services when multiple parties are sharing in the profits.” ALT Title

Tip: As the buyer, you have the right to shop around and choose which independent title insurance/settlement company you want to work with. It's federal law. You're not obligated to go with your lender's recommendation or use your real estate agent's in-house title company. Although title insurance rates are approved by and filed with the PA Department of Insurance, settlement service fees vary greatly from one company to another.

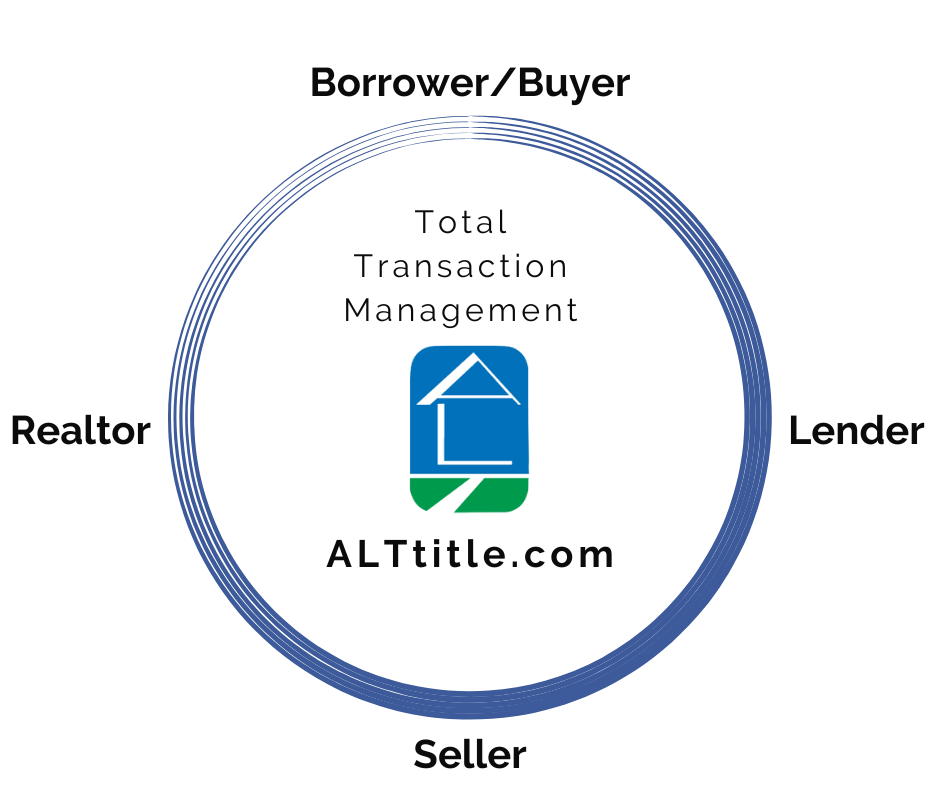

We Manage Your Transaction

And it’s all included in the one-time title insurance premium paid at closing.

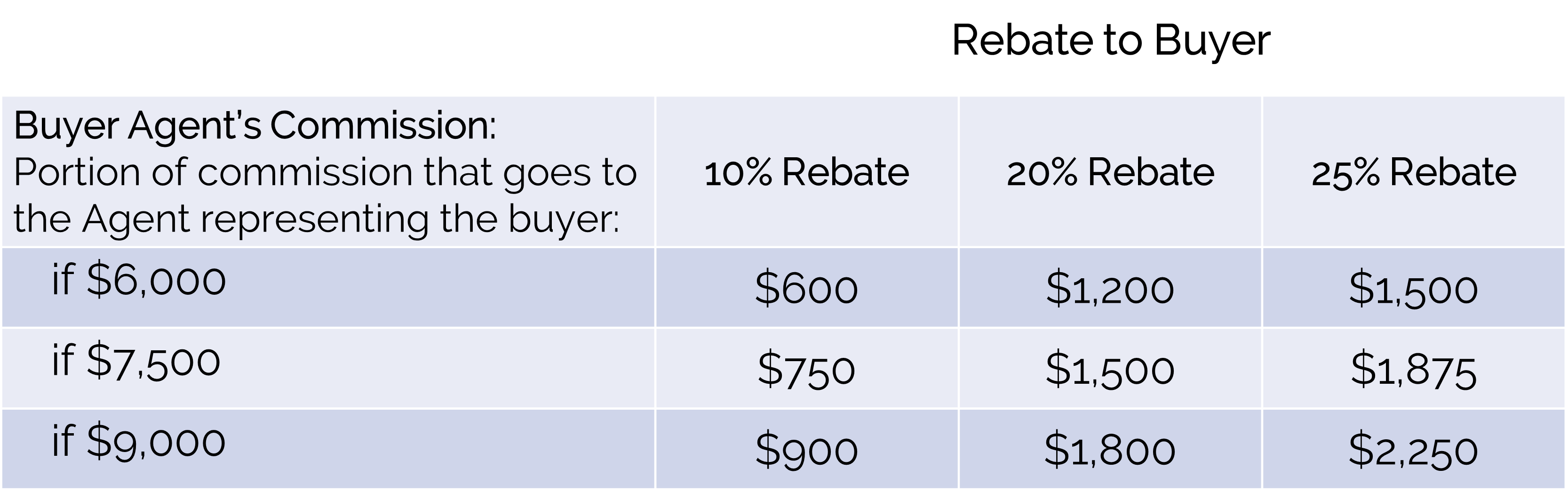

3. Ask your Real Estate Broker for a Commission Rebate.

A real estate commission rebate can save you up to $1,000 or more at settlement.

Fees for professional services are negotiable. Just ask your attorney and they’ll tell you that their clients are always asking for a reduced hourly rate. When it comes to your doctor, in most cases your insurance company negotiated their rates on your behalf. Real estate commissions and admin fees are no different.

The sales commission in most cases is paid by the seller. Buying new construction is no different. As the seller, the builder would be paying a sales commission to your real estate agent. Hiring the right real estate agent to represent you is the key.

Savvy real estate agents and brokers realize that by rebating a portion of their commission to their buyer, they’ll potentially do more business, either by making it possible for someone to afford a house a little sooner than they anticipated, or through additional referrals from satisfied customers. We suggest asking agents if they offer commission rebates during the interview process - before you begin looking at houses.

Tip: Selling one home and buying another? If you’re using the same real estate agent for both transaction, you may be able to reduce or even eliminate the commission typically paid to the listing agent on the sale of your home.

Commission rebates are redeemed one of two ways.

- If you make your lender aware of the rebate, often times they’ll allow it as a credit towards your allowable closing costs at settlement.

- If the rebate exceeds the maximum credit toward allowable closing costs, due to either a separate lender credit or seller credit, your broker can write you a rebate check once the transaction has closed.

ALT Referrals Done Right

We're redefining the role of the Title Agent.

As a family-owned title insurance and settlement services company, we help you cut through all the BS. We offer you the best deal right up front. And, if you’d like to work with a real estate agent who can offset a portion of your closing costs with a generous commission credit, or a local lender who offers great rates without a lot of fees, we’d be happy to make the no obligation introduction. It really is that easy!

Most transparent and fastest worry-free service I could have ever imagined.

"They were able to process everything in a record span of 11 days where I have heard other title companies take 30 days. Also, no hassle pricing with clear cost of valid things. No unnecessary asks. They keep it simple, Clear, efficient and fast. Much recommended."

-Ankur Jain

Highly recommended!

"Remortgaging can be such a hassle. We knew it made sense but hated to have to go through all the paperwork as well as find a mortgage agent/broker. Frank connected us with a fantastic broker. Our settlement experience with Alt Title was the easiest remortgage we have ever been through. The offices are bright, updated and so clean! We were greeted with a very friendly smile as soon as we walked in the door. Frank and his team made the process as easy as it could’ve been."

-Kara Raudenbush

Closing my home purchase with ALT Title was a real pleasure.

"Their straightforward quote system makes it easy to price title with no hidden fees. When we needed to use a power of attorney, they were extremely helpful and I appreciate that they did not use this as an opportunity to upcharge. I am happy I chose to go with ALT rather than my broker's in-house agency. I would not hesitate to use ALT Title again, and I highly recommend them."

-Teddy Einstein

The Quote Was Unbeatable!

"I was introduced to ALT through my realtor. The quote was unbeatable. No hidden fees at settlement. No surprises at all. They were on time and everything was smooth. Frank answered all the questions patiently and things to avoid after the settlement in regards to duplicate deeds in mail and other cautions. I would recommend ALT to anyone looking for a title company."

-Arvind J

Rare Find

"Just wanted to let you know that I would highly recommend your company for Title and Closing Services. You customer service, efficiency, follow-up, and knowledge is second to none. In this day an age it is rare to find a company with your level of service."

-Don S.

Top Notch!

"The staff at ALT Title are all top notch professional, knowledgeable, and friendly employees. The seller’s attorney was difficult to communicate with and late delivering documents. Even with these delays, ALT Title kept up communications, kept things moving and we SETTLED ON TIME."

-Tim and Nicole Christian

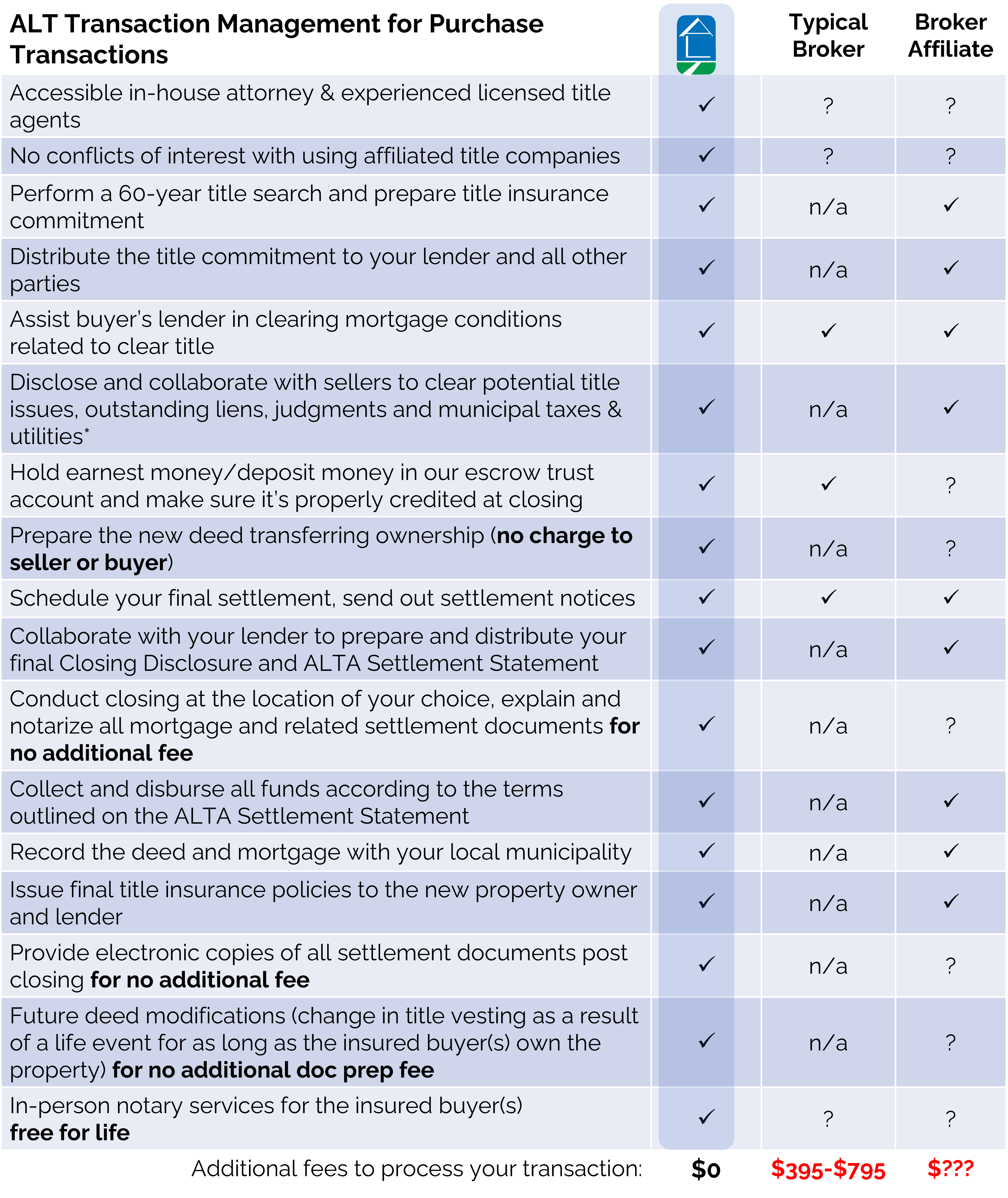

4. Ask your Real Estate Broker to waive their Admin Fee

Save from $395 to $795 by eliminating a fee for transaction management.

Today, as a result of technology and streamlined processes, these fees seem to be a little outdated and agents/brokers who eliminate these unnecessary fees for their customers enjoy a competitive advantage in an ever changing market.

If your real estate agent/broker, or their title insurance affiliate, typically charges the buyer an administrative fee (also referred to as a broker service fee or conveyancing fee) to manage the transaction, ask them to waive it. Eliminating this fee alone can save you an additional $395 to $795. The reality is that under federal law, the buyer is not required to purchase this service as part of their transaction. View a sample Conveyancing Addendum.

Tip: When you're buying a home and hire ALT to provide title insurance and settlement services, we don’t charge you an additional fee to manage the transaction. The list of services that we perform on your behalf far exceeds the conveyancing services offered by most real estate brokers and it’s all included in the one-time title insurance premium that you’ll pay at closing.

Buying AND Selling? If selling one house and buying another, both in PA, when you choose ALT to provide the title insurance and settlement services for your new home, we’ll also assist you with clearing title on the house that you're selling at no additional charge, potentially saving you $300 or more for this service offered by many real estate brokers. This includes, ordering the mortgage payoff and the required certifications. The only thing that you’ll pay is the actual amount for the necessary certifications charged by your homeowners association or municipal authority.

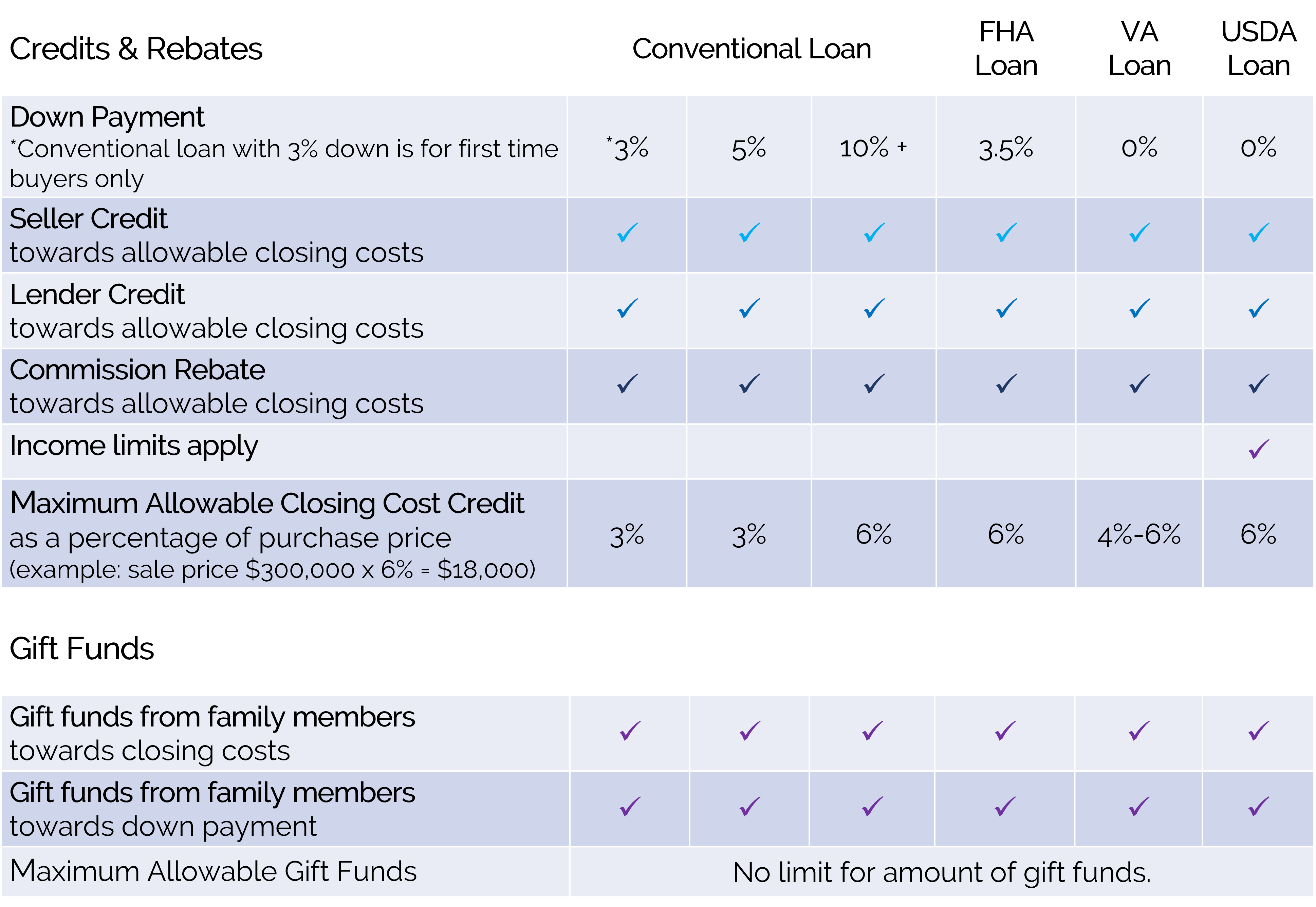

5. Seller Credits & Gift Funds from Family

Depending on your loan program, allowable credits and rebates will vary.

A seller credit or gift funds from a family member (or a combination of the two) could save you thousands of dollars and even eliminate all of your out of pocket costs.

As we transition into a new real estate market, it’s becoming a little easier for buyers to ask the seller for assistance with covering some or even all of the buyers allowable closing costs. In-fact, the seller can even pay to buy down your mortgage interest rate for the first two years so that you can ease into home ownership with a lower interest rate and monthly payment. Working with an experienced lender will be essential to structuring the transaction to maximize the amount of seller credit allowable.

Another option to reducing the amount of personal cash you’ll need to buy a new home is receiving gift funds from a family member. Unlike seller credits, lender credits and/or commission rebates, there are no limits to the amount of gift funds that you can receive towards the purchase of your new home. Gift funds can be used towards both closing costs and your down payment. Essentially making it possible for you to buy a new house without touching your savings.

When the buyer chooses ALT for their title insurance, both Buyer and Seller in a private transaction can save money at settlement. View a list of our comprehensive services.

Save up to at the settlement table.

No Closing Fee

We Attend Settlement for No Additional Fee

No Miscellaneous Title Fees

No Doc Prep Fees, including Deed and/or POA

No Admin Fees* (learn more)